Snowflake Just Hit 52-Week Lows: Is This the Best Deep Value Setup in Tech Right Now?

SNOW is down 57% from its highs as Wall Street panic-sells the entire SaaS sector. Here’s what the data actually says.

Let me be straight with you: I’ve already started building a position in Snowflake (NYSE: SNOW 0.00%↑ ). I’ve shared this with my subscribers, and now I want to show you exactly why — and exactly what risks you need to understand before you consider doing the same.

This is not a hot take. This is not a momentum play. This is a deep value thesis on a company that the market is treating like a dying business model — when the actual financials tell a completely different story.

The thesis is simple: Wall Street is pricing Snowflake like AI is going to kill it. But AI doesn’t replace the data lake — AI requires it.

Let me break this down.

The SaaSpocalypse: What Happened to Software Stocks

To understand why Snowflake is trading where it is, you first need to understand the broader panic gripping the entire software sector.

In February 2026, Anthropic launched Claude Cowork — a product demonstrating AI agents performing sustained, autonomous knowledge work across legal review, financial analysis, customer support, and project management. Within 48 hours, roughly $285 billion was wiped from SaaS company valuations. The S&P 500 Software & Services Index, which tracks 140 constituents, dropped over 4% in a single session and extended its losing streak to eight consecutive sessions. The index is now down approximately 20% year-to-date.

The market’s logic was straightforward: if AI agents can do the work of five employees, companies need fewer software seats. Per-seat SaaS pricing — the revenue model that powered two decades of software dominance — suddenly looked vulnerable. Thomson Reuters dropped nearly 16% in a single day. LegalZoom cratered almost 20%. Workday and DocuSign were downgraded by Jefferies specifically citing AI disruption.

The selloff was the worst for the iShares Expanded Tech-Software ETF (IGV) since the 2008 financial crisis. Goldman Sachs’ basket of US software stocks fell 6% in a single day.

Here’s the problem: the market painted every software company with the same brush. And that’s where opportunity lives.

Bank of America senior analyst Vivek Arya called the selloff “indiscriminate” and “logically inconsistent.” Even Nvidia CEO Jensen Huang told CNBC the markets got it wrong — arguing that AI is expressed through software, not as a replacement for it. Goldman Sachs CEO David Solomon said the selloff was “too broad,” suggesting the market wasn’t differentiating between companies that would be disrupted by AI and those that would benefit from it.

This distinction is everything when it comes to Snowflake.

What Snowflake Actually Does (And Why It Matters)

If you’re newer to this name, here’s the deal. Snowflake is not a typical SaaS company selling monthly seat licenses. It is a cloud-native data platform — the foundational infrastructure layer where enterprises consolidate, store, govern, and analyze their data across multiple cloud environments.

Think of it this way: every Fortune 500 company has data scattered across AWS, Azure, Google Cloud, on-premise servers, and dozens of legacy systems. Snowflake acts as the single source of truth — a unified data lake and data warehouse that sits across all of those environments and makes the data usable. It’s the plumbing, the foundation, the bedrock.

The company operates on a consumption-based pricing model, not a per-seat model. Customers pay based on the storage and compute they actually use. This is a critical distinction — it means Snowflake’s revenue model is not directly threatened by the per-seat collapse that’s hammering traditional SaaS companies. If anything, as enterprises deploy more AI workloads that need to query more data, Snowflake’s consumption goes up, not down.

Snowflake currently serves over 12,600 customers worldwide, including 790 of the Forbes Global 2000. Once a massive corporation builds its data ecosystem on Snowflake, the switching costs are astronomical. You don’t rip out and replace your entire enterprise data architecture overnight. That is the “sticky” moat.

The Financials: What the Bears Don’t Want You to See

Let’s look at what the business is actually doing while the stock gets taken to the woodshed.

Q4 Fiscal Year 2026 (quarter ending January 31, 2026):

Total revenue: $1.28 billion, up 30% year-over-year

Product revenue: $1.23 billion, also up 30% YoY

Remaining performance obligations (RPO): $9.77 billion, up 42% YoY — this is contracted future revenue that hasn’t been recognized yet

Net revenue retention rate: 125% — meaning existing customers are spending 25% more than they did a year ago

Adjusted free cash flow margin: 61% in Q4

733 customers with trailing 12-month product revenue greater than $1 million, up 27% YoY

56 customers spending over $10 million annually, a 56% increase YoY

The company signed its largest deal in history — a single contract worth over $400 million

Full fiscal year 2026:

Total revenue: $4.7 billion, up 29% from $3.6 billion in fiscal 2025

Non-GAAP operating margin: 10.5%, expanding more than 400 basis points year-over-year

Stock-based compensation declined from 41% of revenue in fiscal 2025 to 34% in fiscal 2026, with guidance to drop further to 27% in fiscal 2027

For FY2027, management is guiding for a 75% product gross margin and a 12.5% operating margin — with analysts expecting the company to hit a meaningful profitability milestone this year. Estimated EPS for fiscal 2027 is projected at $1.77, compared to a net loss of -$3.95 per share last year.

Let me say that again: a company growing revenue at 30%, generating 61% adjusted free cash flow margins in its most recent quarter, with nearly $10 billion in contracted future revenue, is trading at 52-week lows.

The AI Pivot: Snowflake Isn’t Getting Killed by AI — It’s Becoming the AI Infrastructure Layer

This is where the market narrative completely falls apart.

Snowflake has spent the past 18 months aggressively building out Cortex AI — a suite of AI-native capabilities that transform the platform from a data warehouse into the place where enterprises actually build and run their AI applications.

Here’s what’s now live or rolling out:

Cortex Code — an AI coding agent purpose-built for enterprise data stacks, launched in November 2025 and already adopted by over 4,400 users. It now supports dbt and Apache Airflow workflows, effectively working across the entire modern data stack, not just within Snowflake’s walls.

Snowflake Intelligence — an enterprise intelligence agent that lets non-technical users query enterprise data in natural language, getting trusted answers from governed data sources.

Cortex AI for Financial Services — a vertical-specific suite launched with integrations from CB Insights, Deutsche Börse, MSCI, Nasdaq, FactSet, and The Associated Press, enabling financial institutions to run AI workloads on proprietary + third-party data with enterprise-grade security.

Snowflake MCP Server — enabling interoperability with the broader AI agent ecosystem, including Anthropic, Amazon Bedrock, Azure AI Foundry, Salesforce’s Agentforce, Cursor, and many others.

Over 9,100 accounts now leveraging Cortex for tasks from natural language querying to complete ML pipelines, driving 200%+ growth in AI-related workloads.

Here’s the key insight that the market is missing: every AI agent needs data to operate on. When enterprises deploy AI agents for fraud detection, customer analytics, investment research, or operational intelligence, those agents need to access governed, secure, centralized data. Snowflake is that data layer. The more AI agents proliferate across the enterprise, the more compute and storage consumption runs through Snowflake’s platform.

As Sridhar Ramaswamy, Snowflake’s CEO, put it during the Q4 earnings call: Snowflake has spent over a decade building the foundation that makes AI safe and scalable — a single source of truth, cross-cloud interoperability, and enterprise-grade governance. Now they’re activating agentic capabilities on top of that platform.

AI isn’t the enemy here. AI is the next growth engine.

The Bear Case: What You Need to Account For

I’m not going to pretend this is a risk-free setup. It’s not. Here’s what’s working against the stock right now, and you need to have eyes wide open on all of it.

1. GAAP Profitability Remains Elusive

Despite the strong adjusted metrics, Snowflake reported a GAAP net loss of $1.3 billion for fiscal 2026 — roughly in line with the $1.3 billion loss in fiscal 2025. Heavy stock-based compensation remains the primary culprit. Institutional investors are currently avoiding companies that can’t show clean GAAP profitability, and in this risk-off environment, that’s a real headwind.

2. Growth Deceleration

Snowflake’s five-year average revenue growth rate was over 72%. It’s now at 30%. Still excellent by any standard, but Wall Street punishes high-multiple stocks hard when growth decelerates. The question is whether AI-driven workloads can reaccelerate growth, or if 25-30% becomes the new normal.

3. The Lawsuit Overhang

Multiple securities class action lawsuits have been filed against Snowflake, with a lead plaintiff deadline of April 27, 2026. The lawsuits allege that the company failed to disclose that product efficiency gains, Iceberg Tables (an open-source table format), and tiered storage pricing changes would have a material negative impact on consumption and revenues. These are the kinds of ambulance-chaser lawsuits that follow any significant stock decline, but they create uncertainty and legal costs. They need to be acknowledged.

4. Cybersecurity Headline Risk

In 2024, Snowflake was at the center of one of the year’s largest cybersecurity incidents when hackers used stolen credentials to access approximately 165 customer environments that lacked multi-factor authentication. Major names — AT&T, Ticketmaster, Santander — were affected. Snowflake’s own systems were not breached, and the company has since mandated MFA and enhanced its security posture, but the reputational sting lingers.

Just this week, a new third-party incident surfaced: a supply chain attack on analytics company Anodot (acquired by Glassbox in November 2025) resulted in stolen authentication tokens being used to access a small number of Snowflake customer accounts. Snowflake responded quickly, locking down affected accounts and confirming their systems were not compromised — but the headline risk is real and recurring.

5. Competitive Pressure

Snowflake competes with deep-pocketed hyperscalers: Google BigQuery, Amazon Redshift, and Microsoft’s data platform offerings. These competitors can bundle data services with their existing cloud infrastructure at aggressive price points. Snowflake’s advantage is its cloud-agnostic neutrality — it works across AWS, Azure, and Google Cloud — but the competitive landscape is intense and the hyperscalers aren’t standing still.

The Valuation Picture

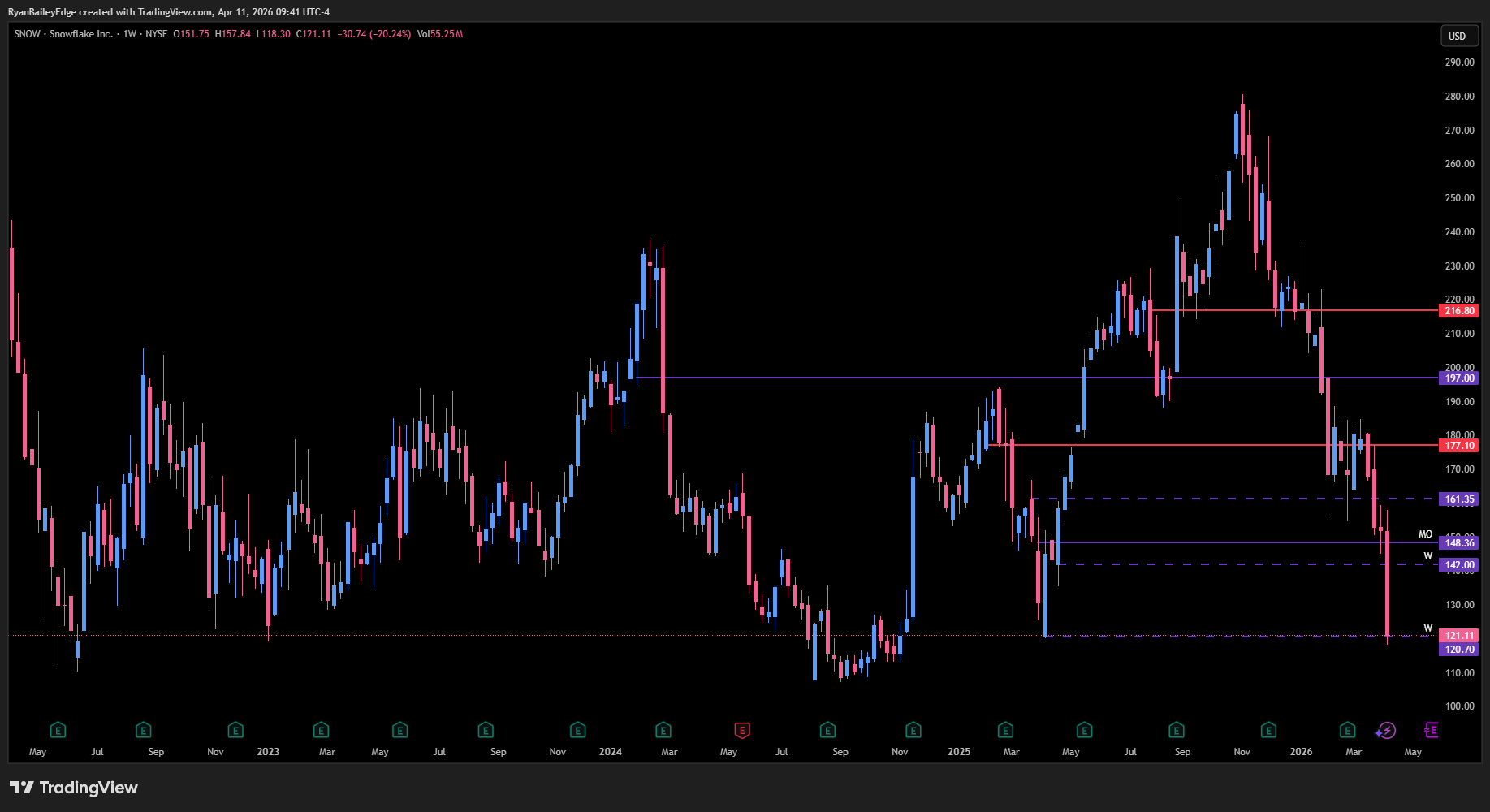

As of the most recent close, SNOW is trading around the $121, down from a 52-week high of $280.67. That’s a decline of over 57%.

The market cap sits at approximately $50 billion. On trailing twelve-month revenue of $4.7 billion, that’s roughly a 10.6x price-to-sales ratio. For a company growing at 30% with 61% adjusted free cash flow margins, that multiple has compressed dramatically from where it’s been historically.

Here’s what Wall Street analysts are saying: 34 out of 37 analysts rate SNOW as Buy or Strong Buy. The average 12-month price target is approximately $235–250, which implies roughly 60-90% upside from current levels. The lowest target among major analysts is $177 (Macquarie), and the highest is $325 (JMP Securities).

The analyst consensus isn’t gospel, but when virtually the entire Street is calling a stock a Buy and it’s still selling off, that tells you the selling is sentiment-driven, not fundamental. This is the kind of dislocation where long-term value gets created.

How I’m Thinking About This

I’ve already started building a position, and I’ve told my subscribers exactly that. Here’s the framework I’m using.

This is not a trade. This is a long-term hold thesis. You’re buying a company that is the foundational data infrastructure for hundreds of the world’s largest enterprises, generating nearly $10 billion in contracted future revenue, pivoting aggressively into AI, and getting priced like the business model is broken.

The smart approach: start small, define your risk, and don’t try to catch the exact bottom. The stock is heavily battered near the $120-130 area, which is acting as a critical support zone near 52-week lows. Because this is a high time-frame setup, you can treat this zone as a deep value area — but respect the price action. If it breaks and holds below $120 convincingly, that changes the risk profile and it turns into a waiting game. Reclaims 130 with confidence and we got something.

What to watch from here:

Next earnings report (estimated late May 2026): This is the catalyst. If AI-driven workload growth accelerates and margins continue expanding, the stock has significant re-rating potential. If growth disappoints, expect another leg down.

Resolution of the lawsuit overhang: The April 27 lead plaintiff deadline will bring clarity. These lawsuits typically take years to resolve but the initial headlines create the most selling pressure.

Broader SaaS sentiment: If the sector-wide panic begins to subside and institutional money rotates back into quality software names, Snowflake will be one of the first to benefit given its fundamental profile.

GAAP profitability milestone: Management is guiding toward meaningful improvement in FY2027. If Snowflake can demonstrate GAAP profitability or a clear path to it, the institutional buyer base expands significantly.

The Bottom Line

The market is telling you that AI kills Snowflake. The data is telling you that AI needs Snowflake. When those two narratives are this far apart, and the company is printing $1.2 billion quarters with $9.77 billion in contracted future revenue, I want to be on the side of the data.

Is there risk? Absolutely. Growth deceleration, lawsuit noise, cybersecurity headlines, GAAP losses, and a hostile macro environment for software stocks are all real. This is why you size appropriately and manage your risk.

But for patient capital with a 12-to-24-month horizon, I believe this is one of the best deep value setups in the technology sector right now. The foundation is there. The data moat is real. The AI pivot is underway. And the price is reflecting maximum fear.

That’s usually when you want to be paying attention.

Until next time—trade smart, stay prepared, and together we will conquer these markets!

Ryan Bailey, VICI Trading Solutions.

Very nice! Thanks for this. Being just a chart/price trader, did have an alert at 126 just in case it were to fall back to it's VAL (period from 2022 through high of 2025) as a casualty of the broader SAAS sell off. And knowing nothing about the fundamentals of this space, nice to hear your thoughts on it.

Glad I could help. I've been wanting to buy this for sometime as I know many people in corporate America whos companies are ballz deep in the snowflake ecosystem and once you are in especially for a large corporation there is no getting out. It's a very sticky business model so this has been attractive to me for a while. TBH I'm happy about this long term opportunity. Glad I could help